- Difference Between Coupon vs Yield

- Relationship between bond prices and interest rates

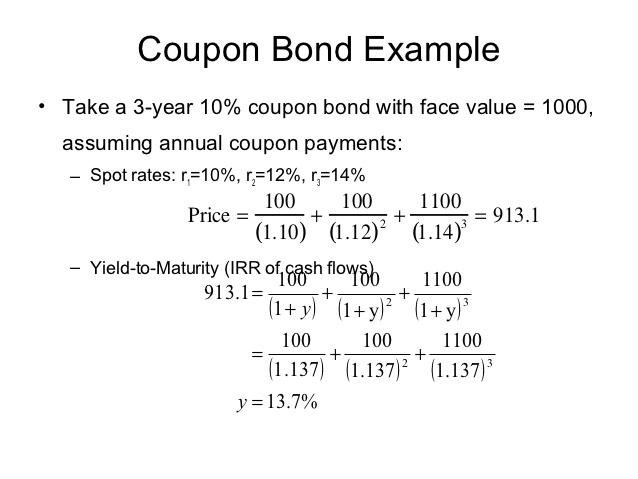

- What is yield and how does it differ from coupon rate?

- Coupon vs Yield

- Categories

Difference Between Coupon vs Yield

In this, A is the protection buyer and B is the protection seller. If the reference entity does not default, the protection buyer keeps on paying bps of Rs 50 crore, which is Rs 50 lakh, to the protection seller every year. On the contrary, if a credit event occurs, the protection buyer will be compensated fully by the protection seller. The settlement of the CDS takes place either through cash settlement or physical settlement. For cash settlement, the price is set by polling the dealers and a mid-market value of the reference obligation is used for settlement.

There are different types of credit events such as bankruptcy, failure to pay, and restructuring. Bankruptcy refers to the insolvency of the reference entity. Failure to pay refers to the inability of the borrower to make payment of the principal and interest after the completion of the grace period. Restructuring refers to the change in the terms of the debt contract, which is detrimental to the creditors.

If the credit event does not occur before the maturity of the loan, the protection seller does not make any payment to the buyer. CDS can be structured either for the event of shortfall in principal or shortfall in interest. There are three options for calculating the size of payment by the seller to the buyer. Fixed cap: The maximum amount paid by the protection seller is the fixed rate. Variable cap: The protection seller compensates the buyer for any interest shortfall and the limit set is Libor plus fixed pay. No cap: In this case, the protection seller has to compensate for shortfall in interest without any limit.

Relationship between bond prices and interest rates

The modelling of the CDS price is based on modelling the probability of default and recovery rate in the event of a credit event. Although used for hedging credit risks, credit default swap CDS has been held culpable for vitiating financial stability of an economy. This is particularly attributable to the capital inadequacy of the protection sellers. Counter-party concentration risk and hedging risk are the major risks in the CDS market. It is the periodic rate of interest paid by bond issuers to its purchasers. For example, if you have a year- Rs 2, bond with a coupon rate of 10 per cent, you will get Rs every year for 10 years, no matter what happens to the bond price in the market.

Description: The government and companies issue bonds to raise money to finance their operations.

What is yield and how does it differ from coupon rate?

When you buy a bond, the bond issuer promises periodic annually or semi-annually interest payments on the money invested at the coupon rate stated in the bond certificate. The bond issuer pays the interest annually until maturity, and after that returns the principal amount or face value also. Coupon rate is not the same as the rate of interest. An example can best illustrate the difference. Suppose you bought a bond of face value Rs 1, and the coupon rate is 10 per cent.

Every year, you'll get Rs 10 per cent of Rs 1, , which boils down to an effective rate of interest of 10 per cent. However, if you bought the bond above its face value, say at Rs 2,, you will still get a coupon of 10 per cent on the face value of Rs 1, It means you'll still get Rs But, since you bought the bond at Rs 2,, the rate of interest this time would only be 5 per cent Rs of Rs 2, Likewise, if you bought the bond below its face value, say at Rs , you'll still receive Rs every year, but this time the interest rate would be 20 per cent Rs of Rs Popular Categories Markets Live!

Or you could just essentially say that the bond would be trading at a discount to par. Bond would trade at a discount, at a discount to par. Now, let's say the opposite happens. Let's say that interest rates go down.

- jiffy lube coupons utah safety emissions!

- scott toilet paper coupon codes!

- These metrics for calculating investment returns have completely different uses..

- coupon tria laser hair removal!

- amazon cyber monday cd deals!

- outback steakhouse online ordering coupons!

Let's say that we're in a situation where interest rates, interest rates go down. So how much could you sell this bond for? I'm not being precise with the math.

Coupon vs Yield

I really just want to give you the gist of it. So now, I would pay more than par. Or, you would say that this bond is trading at a premium, a premium to par. So at least in the gut sense, when interest rates went up, people expect more from the bond. This bond isn't giving more, so the price will go down. Likewise, if interest rates go down, this bond is getting more than what people's expectations are, so people are willing to pay more for that bond. Now let's actually do it with an actual, let's actually do the math to figure out the actual price that someone, a rational person would be willing to pay for a bond given what happens to interest rates.

And to do this, I'm going to do what's called a zero-coupon bond. I'm going to show you zero-coupon bond.

- pot seeds coupon!

- What is a Discount Bond?.

- amc movies coupon codes!

- great ocean road deals!

Actually, the math is much simpler on this because you don't have to do it for all of the different coupons. You just have to look at the final payment. There is no coupon. So if I were to draw a payout diagram, it would just look like this. This is one year. This is two years. Now let's say on day one, interest rates for a company like company A, this is company A's bonds, so this is starting off, so day one, day one.

The way to think about it is let's P in this I'm going to do a little bit of math now, but hopefully it won't be too bad. Let's say P is the price that someone is willing to pay for a bond. Let me just be very clear here. If you do the math here, you get P times 1. This is 1. So what is this number right here? Let's get a calculator out. Let's get the calculator out. If we have 1, divided by 1. Now, what happens if the interest rate goes up, let's say, the very next day? And I'm not going to be very specific.

I'm going to assume it's always two years out. It's one day less, but that's not going to change the math dramatically.

Categories

Let's say it's the very next second that interest rates were to go up. Let's say second one, so it doesn't affect our math in any dramatic way. Let's say interest rates go up. So now all of a sudden, so interest, people expect more. Interest goes up. We'll use the same formula. We bring out the calculator.

We bring out the calculator, and I think you have a sense we have a larger number now in the denominator, so the price is going to go down.